Fixed assets are a vital piece of the accounting puzzle, shedding light on a company’s financial well-being and stability. Grasping the concept of fixed assets is crucial for businesses big and small, so we’re diving deep into their importance, classification, valuation, and accounting treatment. Whether you’re a business owner, an accounting student, or just curious about financial lingo, this guide will equip you with the fundamentals of fixed assets.

What are Fixed Assets in Accounting?

Imagine fixed assets as the trusty sidekicks of a business, always ready to help generate income without needing to be sold off. Also known as tangible assets, these long-term resources stick around for the long haul, providing benefits across multiple accounting periods – usually more than a year. We’re talking about the property, plant, and equipment (PP&E) like land, buildings, machinery, vehicles, furniture, and fixtures that make the magic happen behind the scenes as a company churns out goods and services.

Classifying and Valuing Fixed Assets

Now that we’ve established the significance of fixed assets, let’s dive into their classification and valuation. Fixed assets are classified into various categories, such as land, buildings, machinery, equipment, and vehicles. This classification helps businesses manage their assets more effectively and make informed decisions about their acquisition, maintenance, and disposal.

Valuing fixed assets is also essential, as it enables companies to determine their worth and depreciation. Typically, fixed assets are recorded at their initial cost, which includes the purchase price plus any additional expenses incurred to get the asset ready for use. Over time, the value of fixed assets decreases due to wear and tear, technological advancements, or market fluctuations. This reduction in value is called depreciation, and it’s a crucial aspect of accounting for fixed assets.

- Long-term Investments as Fixed Assets: When it comes to long-term investments, you might have heard the term fixed assets thrown around. But what exactly are they? Well, these are investments that meet specific criteria and are typically held onto for an extended period, rather than being intended for a quick sale. Think stocks, bonds, or even real estate properties that generate rental income. However, the way these fixed assets are valued and accounted for can vary based on accounting standards and industry practices.

- Tangible Fixed Assets: Ever wondered what those big-ticket items on a company’s balance sheet are? Say hello to tangible fixed assets, or property, plant, and equipment (PP&E)! These are the physical, touchable assets that make up a business’s backbone – think real estate, machinery, vehicles, and even furniture. They’re kind of a big deal, as they’re vital for keeping operations running and bringing in that sweet, sweet revenue. Now, when it comes to accounting for these hefty assets, there’s a bit of a process involved. First, you’ve got to record their initial cost, and then comes the fun part: calculating depreciation over their useful lives. And just like that, you’ve got tangible fixed assets accounted for and ready to rock on your balance sheet!

- Depreciation: The Silent Warrior: Depreciation is a critical concept when it comes to tangible fixed assets. It reflects the systematic allocation of an asset’s cost over its useful life, accounting for its wear and tear, obsolescence, and natural deterioration. By depreciating assets, businesses accurately report the decline in value of these assets on their balance sheets, providing a realistic picture of their financial standing.

- Intangible Fixed Assets, the Invisible Powerhouses: As we navigate the digital age, intangible fixed assets are stealing the spotlight. Though they may not have a physical presence, these assets pack a powerful punch in the form of intellectual property, patents, copyrights, trademarks, and goodwill. They play a vital role in a company’s competitive edge and long-term triumph. So, how do we account for these intangible wonders? It’s all about assessing their fair value, useful life, and the ever-important amortization process. By doing so, we can truly appreciate the value they bring to the table.

- Amortization: Uncover the true value and significance of assets: Think of amortization as the intangible counterpart to depreciation, which deals with tangible assets. It’s all about the systematic breakdown of an intangible asset’s cost throughout its useful life. Amortizing intangible assets helps businesses track their diminishing value and maintain precise financial reporting. Recognizing amortization expenses on financial statements is key to showcasing a company’s true profitability and how well they’re utilizing their assets.

Importance of Fixed Assets on the Balance Sheet

Imagine the power of fixed assets shaping a company’s balance sheet! Nestled under the noncurrent assets section, these long-term treasures reveal the company’s financial prowess, solvency, and ability to tackle long-term obligations. But wait, there’s more! Fixed assets hold the key to unlocking crucial financial ratios like return on assets and debt-to-equity ratio, offering a sneak peek into a company’s profitability and financial stability.

Current vs. Non-current Fixed Assets: The Time Divide

Differentiating between current and non-current fixed assets is essential to gauge the liquidity and financial flexibility of a company. Current fixed assets are those expected to be turned into cash or used up within one operating cycle, typically a year. On the other hand, non-current fixed assets enjoy a longer life and serve a strategic purpose in a company’s operations. Understanding this distinction empowers businesses to effectively manage their working capital and make informed investment choices.

Depreciable vs. Non-depreciable Fixed Assets: The Wear and Tear Dilemma

When it comes to fixed assets, distinguishing between depreciable and non-depreciable assets is vital. Depreciable fixed assets, such as machinery or vehicles, experience physical wear and tear or a decline in value over time, requiring regular maintenance. In contrast, non-depreciable fixed assets like land don’t depreciate, as their value tends to appreciate or remain constant over time. This classification helps businesses evaluate the financial impact of their assets and make informed decisions regarding maintenance, replacement, or disposal.

Valuation of Fixed Assets

Valuing fixed assets is a critical aspect of accounting, as it determines their worth and presents an accurate picture of a company’s financial position. Fixed assets can be valued using various methods, including historical cost, fair market value, net realizable value, or the cost model. The choice of valuation method hinges on industry practices, accounting standards, and the company’s specific circumstances.

Historical Cost

This straightforward method records fixed assets at their original purchase cost but may not reflect their true value over time due to factors like depreciation or appreciation.

Fair Market Value

This approach determines fixed assets’ value based on their current market price, providing a more realistic valuation. It’s commonly used when assets are bought or sold.

Depreciated Replacement Cost

This method considers the cost of replacing an asset with a similar one after accounting for depreciation. It’s useful for estimating an asset’s economic value at a specific point in time.

Income Approach

This approach assesses the future income-generating potential of fixed assets to determine their value, often used for specialized assets like intellectual property or patents.

Accounting Treatment of Fixed Assets

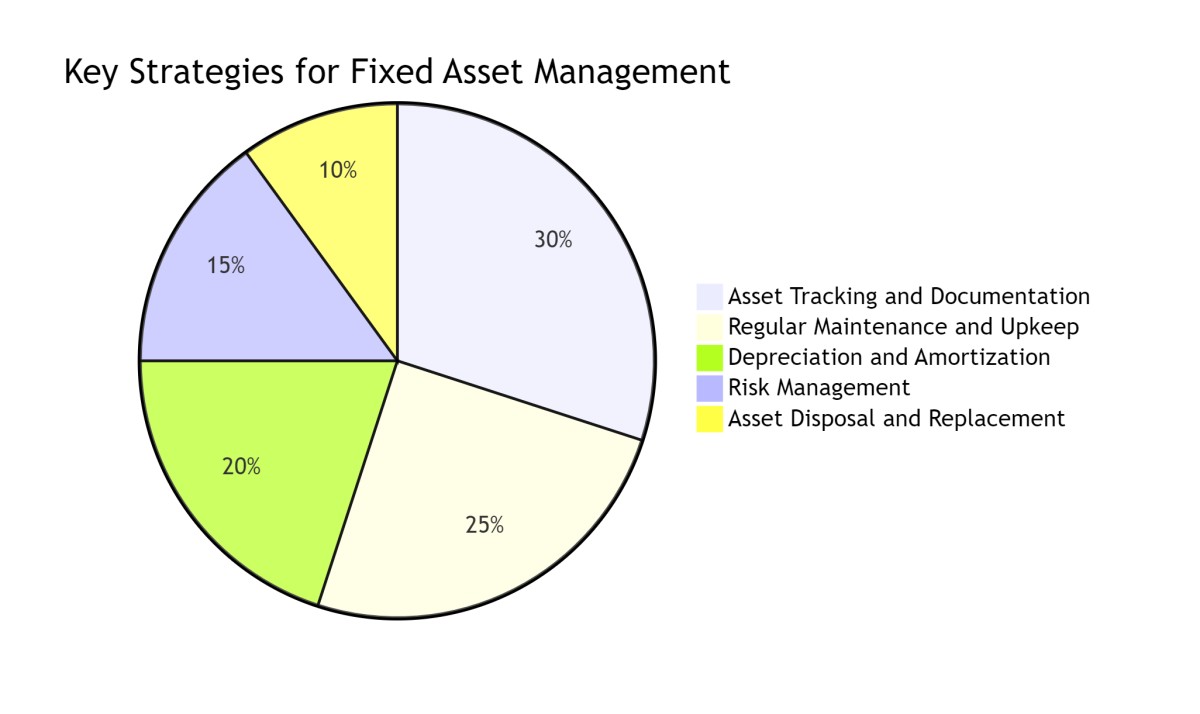

Proper accounting treatment of fixed assets ensures accurate financial reporting and compliance with accounting standards. The key aspects of accounting treatment for fixed assets include:

Asset Tracking and Documentation

Maintain a comprehensive inventory of all fixed assets, including detailed information such as purchase date, cost, location, and depreciation schedule. Utilize asset management software or specialized tools to streamline the tracking process, minimize errors, and enhance efficiency.

Regular Maintenance and Upkeep

Implement a proactive maintenance program to ensure that fixed assets are kept in optimal condition. Regular inspections, repairs, and replacements can extend the useful life of assets, minimize downtime, and reduce overall costs.

Depreciation and Amortization

Accurately calculate and record depreciation or amortization expenses in compliance with accounting standards. This ensures that the financial statements reflect the gradual consumption of the asset’s value over time.

Risk Management

Mitigate risks associated with fixed assets by implementing appropriate insurance coverage, conducting regular risk assessments, and adhering to safety regulations. This protects the business from potential financial losses due to damage, theft, or accidents.

Asset Disposal and Replacement

Develop a well-defined process for asset disposal, including selling, scrapping, or donating assets that are no longer needed. Additionally, establish criteria for evaluating when assets should be replaced to maintain operational efficiency and keep up with technological.

Conclusion

Fixed assets form the cornerstone of a company’s financial stability and are vital for accurate financial reporting. Understanding the nuances of balance sheets, long-term investments, depreciation, and various asset classifications is crucial for businesses and individuals alike. By breaking down the complexities of fixed assets in accounting, link4solution hope to empower you to make informed financial decisions and pave the way for long-term success.

Remember, the world of accounting may be complex. But with a firm grasp on fixed assets, you can navigate these waters with confidence and achieve your financial goals.