Auditing under GST is a critical exercise aimed at verifying the accuracy of a registered dealer’s financial records and compliance with GST laws. This process ensures the correctness of the GST turnover declared, tax payments made, and refunds claimed.

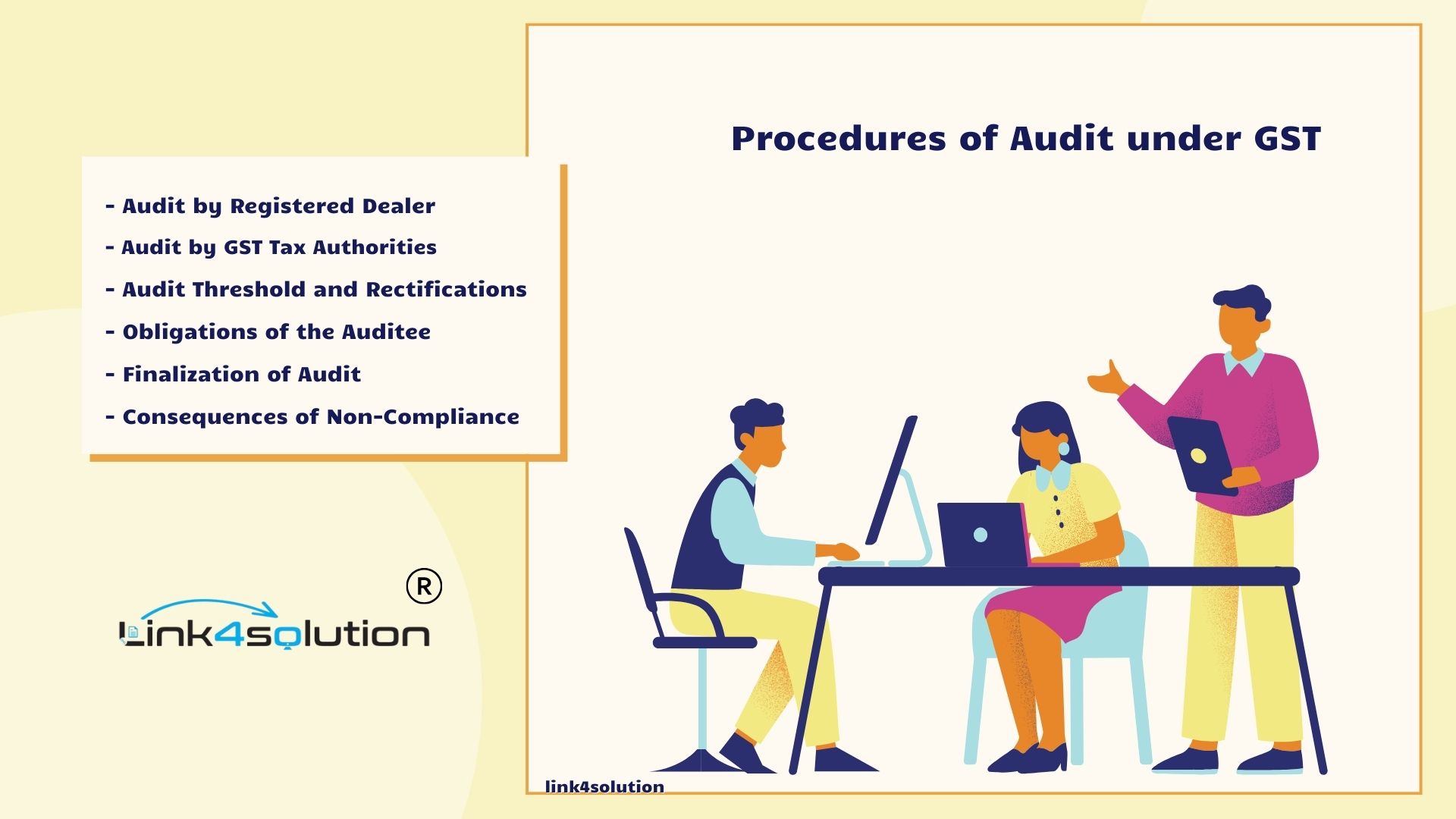

CONTENTS:

– Audit by Registered Dealer

– Audit by GST Tax Authorities

– Audit Threshold and Rectifications

– Obligations of the Auditee

– Finalization of Audit

– Consequences of Non-Compliance

Audit by Registered Dealer:

A registered dealer whose turnover exceeds Rs. 2 crore during a financial year is mandated to have their accounts audited by a Chartered Accountant (CA) or a Cost and Management Accountant (CMA). They must electronically submit their annual return along with the audited financial statements and a reconciliation statement in Form GSTR-9C.

Audit by GST Tax Authorities:

General Audit:

Conducted by the commissioner or an authorized officer, this audit starts with a 15-day prior notice and should be completed within 3 months, extendable by another 6 months.

Special Audit:

Initiated under circumstances where there are discrepancies in the declared values or credit claims, this audit is conducted by a CA or CMA nominated by the commissioner. The audit report must be submitted within 90 days, extendable by another 90 days.

Audit Threshold and Rectifications:

Businesses with turnover exceeding Rs. 2 crore must audit their accounts and file their annual return using Form GSTR 9/9B by December 31 of the next financial year. They must also submit a certified reconciliation statement in Form GSTR-9C.

Obligations of the Auditee:

During an audit, the auditee must provide necessary information, facilitate account verification, and assist in the timely completion of the audit. They should also respond to any discrepancies noted during the audit.

Finalization of Audit:

The audit findings are finalized after considering the auditee’s responses to the observations made. The registered person is informed of the final observations and the consequential actions within 30 days of the audit’s conclusion.

Consequences of Non-Compliance:

Non-compliance with GST laws can lead to severe penalties, including monetary fines and prosecution. The penalty could be as high as Rs. 10,000 or the tax evasion amount, whichever is greater. Continuous offenses can attract additional daily fines.

The intent behind these strict measures is to encourage compliance and maintain transparency under the GST regime. It’s always better to comply proactively with GST laws to avoid penalties and contribute to a more transparent taxation system.